Sand Spring Advisors LLC

There is no one closer to the heart of the recent Internet mania than the fellows who make prices on stocks every day -- either as upstairs Nasdaq market-makers or on the floor as Specialists. In addition, the day-to-day market-makers and Specialists on equity options see some interesting flows. Both groups tend to know who is buying and who is selling, how this business is being executed, and the trading patterns specific to each of their assigned stocks.

With this in mind, and in preparation for a longer article that will shortly appear in Derivatives Strategy magazine, we recently visited the floor of the American Stock Exchange. We spent the day there with Mike Riley, the senior New York partner for Letco Specialists LP, an option market-making firm assigned 105 stocks. The group has a specific high tech focus, trading options on such stocks as Yahoo, Priceline.com, Xilinx, Nextel, and Applied Material, among many others.

What struck us during this visit - more than anything else - were the stories we heard of options being used to blatantly manipulate the price of stocks and often to skirt insider trading restrictions. These stories were nothing short of appalling, and the fact that the SEC seemingly does nothing to investigate them, is even more appalling. As a matter of background, we thought it worth a moment to share three such stories with you.

In late 1999, Riley was trading options on Yahoo, a stock he has since handed on to another Letco partner to look after. Trading was generally pretty volatile one Friday, with Yahoo rallying up $7 dollars or so in the morning to trade around $183. It was an expiration day, and toward 3:30 p.m., the stock had made it up to $186. With 15 minutes to go to the close, the stock was still well under the $190 strike.

"Then, with just a few minutes to trade, a big retail customer came in looking for the $190 calls," says Riley. "Chicago was offering them at 7/8. We were bidding $1 trying to lift Chicago's 7/8 offer, but its not always easy to buy from another market maker. There is no electronic link between us; you have to call the order in over the phone. Just to be competitive with Chicago, we sold the customer 200 at 7/8th. -- a trade we almost felt like throwing up on. We finally got Chicago up to 1 bid, when the customer plows in and buys 2000 up to 2, then another 1000 up to 2 1/2, and then the last 1000 on both exchanges at 5."

Every specialist and market maker was scrambling to buy stock at the same time, and the stock was now trading $190 ½ at the close.

"You might think net of the premiums we had received, that we had won," sighs Riley. "But we couldn't buy any stock --hardly a single share. Then the stock traded up to $194 1/2 in the aftermarket on no size and opened $199 on Monday, before vaulting up to $206. Just as I'm sure the CBOE was, we got run over. That 2-minute bet on our part ended up costing us over $1 million."

Was this retail customer trying to purposefully manipulate the stock using options? Might this type of behavior have been reportable to the SEC?

"In that specific instance, I'm not so sure it was anything other than a wild day at expiration," Riley demurs, "but we see options get used all the time in potentially devious and illegal ways."

Riley then tells the story about another of Letco's stocks, Summit Technology (BEAM), that recently became a takeover target:

"Two days before that takeover announcement, one broker came plowing in wanting to do a most unusual spread trade - selling the June 12 puts and buying the in-the-money June 10 calls. The entire package had something like a 160% delta. Then, boom, the takeover is announced two days later. Now tell me that customer didn't know something."

Letco reported the odd trading to the authorities, but Riley doubts if the SEC will do anything about it. "It's just another complaint from a group of people - the specialists - that the government is not sure they even want to exist. No one really cares when we get picked off."

On a grander conspiratorial note Riley goes on to describe the option trading in Priceline.com options when they were first listed. None of the exchanges trade options on a new IPO until at least 90 days have gone by from their initial offering, but on the 91st day, the AMEX was preparing for options trading on Priceline, and Letco was named to manage it.

"I should have seen it coming quicker," Riley looks back. "We had requests for Flex customized options before we even started trading the standardized options. That should have been the tip-off that insiders were selling. It took the stock falling fifteen dollars before I realized what was going on, but it's clear now that insiders were huge buyers of puts and sellers of calls."

Riley does not know all the ins and outs of what was allowable for Priceline.com insiders to do under their lock-up covenants, but he is adamant that "they somehow found an outlet to hedge their stock holding using options."

"Within a month's time, I'd estimate that 10 million shares were synthetically sold using options," he states. "Of course the skew to puts was incredible, and it was next to impossible to borrow the stock. The whole thing continued that way for the longest time until the secondary stock offering at $67...Then the stock became easier to borrow and the vols normalized somewhat."

On the day that we are talking with Riley, Priceline.com was trading all the way down at 38 ½, and technically had become oversold. Basis its Fibonacci rhythm, Sand Spring Advisors even put out a Chart du Jour buy recommendation on this latter date, looking for a healthy bounce (since achieved).

But subsequent to our conversation with Riley, Sand Spring Advisors has done a bit more investigation into the earlier period that Riley was referring to.

Priceline.com first went public on March 29, 1999, issuing just 10 million shares to the public (from total shares outstanding of 142,320,427 plus 54,059,902 exercisable options and warrants - real gents these insiders were, keeping the public float that artificially small). By the terms of its original prospectus, insiders were specifically prohibited from selling their restricted shares for six months. Here we quote from the prospectus:

"For a period of 180 days after the date of this prospectus… [holders of restricted stock] will not, without the prior written consent of Morgan Stanley & Co. Incorporated, directly or indirectly, offer to sell, sell or otherwise dispose of any shares of common stock."And yet, we are told by the specialist trading options on Priceline.com that there was absolutely huge buying of puts and selling of calls just 91 days after the IPO - a trend that continued all the way to the secondary stock offering on August 11th. Note that the terminology used above does not include any reference to trading options - an obvious loophole somebody left open.

On the chart below, we have marked the beginning and end of this period from 91 days after the IPO to the secondary offering, together with some other events in the life cycle of Priceline.com.

Note how immediately after listed options came into existence, Priceline.com took it on the chin all the way until its secondary stock issuance at $67 a share, just as Mr. Riley remembered. Note as well that when the largest block of outside stock - held by General Atlantic Partners and Paul Allen's Vulcan Ventures -- became free to trade after May 8, 2000, the stock almost halved in value once again. The second occurrence could just have been a coincidence, but the first dumping of this stock almost assuredly was not.

Now most of this is all ancient history of course. We discuss it simply from an academic point of view of what insiders can and are doing. In the Priceline instance, the prospectus read "no selling of restricted stock before 180 trading days," but it specifically did not say anything about trading listed options. All the holders of restricted stock had to do was to buy puts and sell calls with maturities set three or four months out from the 91st. day of trading, and voila, the insiders were able to synthetically sell their stock early and at good levels. The lock-up covenants technically were not broken. Only the spirit of these rules was obfuscated by using derivatives.

These insiders then had the added gall to launch a secondary offering at $67 so as to sell yet more of their restricted stock (75% of that offering being sold out of private hands, not by the company's treasury). Given all of this, you have to believe that this management team knew exactly what they were doing: taking the public to the cleaners as fast and most assuredly as they could.

But with Priceline.com as a good past example of insider trading at work, where do we look for current clues of insider activities and avarice?

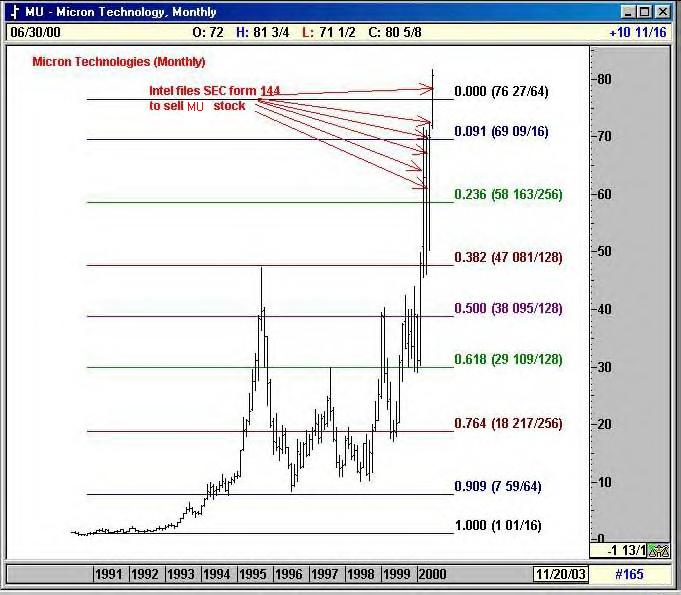

The above chart is of Micron Technologies, a company that has continued to be one of the high-cap darlings of the recent bull market and of which Intel has held a significant investment position - at least until recently. From May 4th forward, a series of Form 144's have been filed by Intel - all intentions to sell stock. Between their first filing on May 4th and now, a total of $505 million of Micron has been sent by Intel to the auction block.

Does this make any sense when Intel is publicly talking about a shortage of DRAM chips being the only limiting factor to their current business performance? If there really was such a shortage, wouldn't Intel be holding on to their Micron investment given that the stock of Micron typically trades with a strong correlation to the price of DRAM semiconductors?

Behind the scenes, Intel of course is now suffering from the reverse syndrome of what has saved them from the prior wrath of Wall Street : managed earnings from gains in their investment portfolio of Internet stocks. In past quarters, operating income has typically been flat, but Intel could always make or beat its earnings expectations by cashing in some of its vast equity portfolio. In the words of Fred Hickey of the High Tech Strategiest:

"Last quarter, revenues were $200 million less than expected, but Intel still "beat" estimates primarily because they told analysts to model approximately $500 million in 'other income.' but actually reported $640 million. For the prior quarter (Q4), Intel guided analysts to $280 million in gains, but reported $508 million."The only problem of course is that Internet stocks collapsed in April and May, sending the value of Intel's portfolio into a nose-dive. How much their portfolio is down is anyone's guess of course, but if it previously had an accumulated $7.8 billion appreciation as of March 31st, Hickey believes that it may have lost as much as two-thirds of that value - or a loss of $5 billion. That sounds high to us, but it is a hard number to track down and prove.

One of Intel's few holdings still with large gains appears to be Micron. Hence the order may well have been given (no doubt) to cash in those holdings to help hide some of the other devastation.

It's all just more example of accounting smoke and mirrors, as it has been for sometime. Previously it was Intel using Internet gains to hide core weakness in its processing-chip business. Now its Intel helping to goose up the semiconductor stocks with talk of DRAM chip shortages, while they quietly cash in their stock holdings.

Somehow - eventually -- the reported gains in this "other income" column will of course have to slow, and that time is now quickly approaching. Intel's true recurring operating results, that are no better than mediocre, will show through. When that day comes, it will not be pretty.

Micron, meanwhile, has for the moment overshot its natural Fibonacci rhythm -- but not by much. Together with Intel's recent filings, scores of other insiders and institutional holders of the company have recently been selling.

If equities do have another leg left to the upside (which basis the NYA and Value Line indices we still see as likely, despite the obvious longer-term stupidity of such an event), we doubt that Micron will be able to maintain its position of relative strength within that final advance. Instead, Micron is more likely to be yet another example of when the insiders take advantage of a naive public. Micron's current $44 billion valuation is nothing short of a joke, and from all appearances, the insiders already know it.

| Corporate Office: 10 Jenks Road, Morristown, NJ 07960 Phone: 973 829 1962 Facsimile: 973 829 1962 |

Best Experienced with

The material located on this website is also the copyrighted work of Sand Spring Advisors LLC. No party may copy, distribute or prepare derivative works based on this material in any manner without the expressed permission of Sand Spring Advisors LLC

This page and all contents are Copyright © 2000 by Sand Spring Advisors, LLC, Morristown, NJ